The income tax or national tax is one of the main ways in which governments collect resources to finance their projects and investments. In Japan, the income tax is known as Shotokuzei and is applied to all individuals and companies that receive an income above a certain annual limit. In this article, we will explore what Shotokuzei is, who needs to declare it, what the tax rate is, and how to declare it.

Contents 5

What is Shotokuzei?

Shotokuzei is a progressive income tax that is applied to all individuals and companies that receive an income above a certain annual limit.

This tax is one of the main sources of revenue for the Japanese government, being used to finance a series of public projects and programs, from infrastructure to social programs.

The word "shotokuzei" (所得税) is composed of two Japanese ideograms: "sho" (所), which means "possession" or "property," and "toku" (得), which means "obtaining" or "acquisition," and "zei" (税), which means "tax." Together, these ideograms form the term that means "income tax."

The origin of the term "shotokuzei" dates back to the early 20th century when Japan began implementing a modern tax system, following the Western model.

In 1922, the first income tax law of the country was enacted, establishing the foundations of the system that is still in effect today. It is a civic obligation and a means of financing government activities.

What is the rate of Shotokuzei?

The rate of Shotokuzei is progressive and varies according to the taxpayer's annual income. The higher the income, the higher the rate applied. The rate table is updated annually by the Japanese government and can be found on its official website.

For illustration, in 2022, the rates range from 5% to 45%, depending on the income bracket. See below a table with the tax percentage according to the income of each Japanese citizen.

| Annual income range | Rate |

|---|---|

| Up to ¥1,950,000 | 5% |

| From ¥1,950,001 to ¥3,300,000 | 10% |

| From ¥3,300,001 to ¥6,950,000 | 20% |

| From ¥6,950,001 to ¥9,000,000 | 23% |

| From ¥9,000,001 to ¥18,000,000 | 33% |

| From ¥18,000,001 to ¥40,000,000 | 40% |

| Above ¥40,000,000 | 45% |

The rate is applied to the taxpayer's taxable net profit, that is, the difference between taxable revenues and expenses throughout the fiscal year.

It is important to remember that these rates may change annually; we recommend checking the information on the official government website or with a professional.

What can be deducted from Japanese income tax?

There are several deductions allowed by law that can be used to reduce income tax in Japan. See below some examples:

- Personal deduction: An automatic and standard deduction of ¥480,000 is allowed for each taxpayer, which is reduced by ¥8,000 for each ¥1,000,000 of taxable income above ¥24,000,000. Additionally, additional deductions are allowed for dependents, spouses, and elderly parents living with the taxpayer.

- Medical expenses deduction: It is possible to deduct medical and dental expenses paid during the fiscal year, up to a limit of ¥100,000 per person. This includes expenses for medical consultations, treatments, exams, medications, among others.

- Education deduction: Deductions for education expenses, such as school tuition, books, teaching materials, among others, are allowed. The limit for this deduction is ¥120,000 per person.

- Donation deduction: It is possible to deduct donations made to non-profit organizations, up to a limit of 40% of the taxpayer's taxable income.

- Health insurance and social security contributions deduction: Contributions to health insurance and social security are also deductible, up to the maximum limit established by law.

- Private pension deduction: Contributions to private pension plans can also be deducted, as long as they are within the limits established by law.

There are other specific deductions for certain types of income and expenses, such as rents, mortgage loan interest, housing expenses, among others.

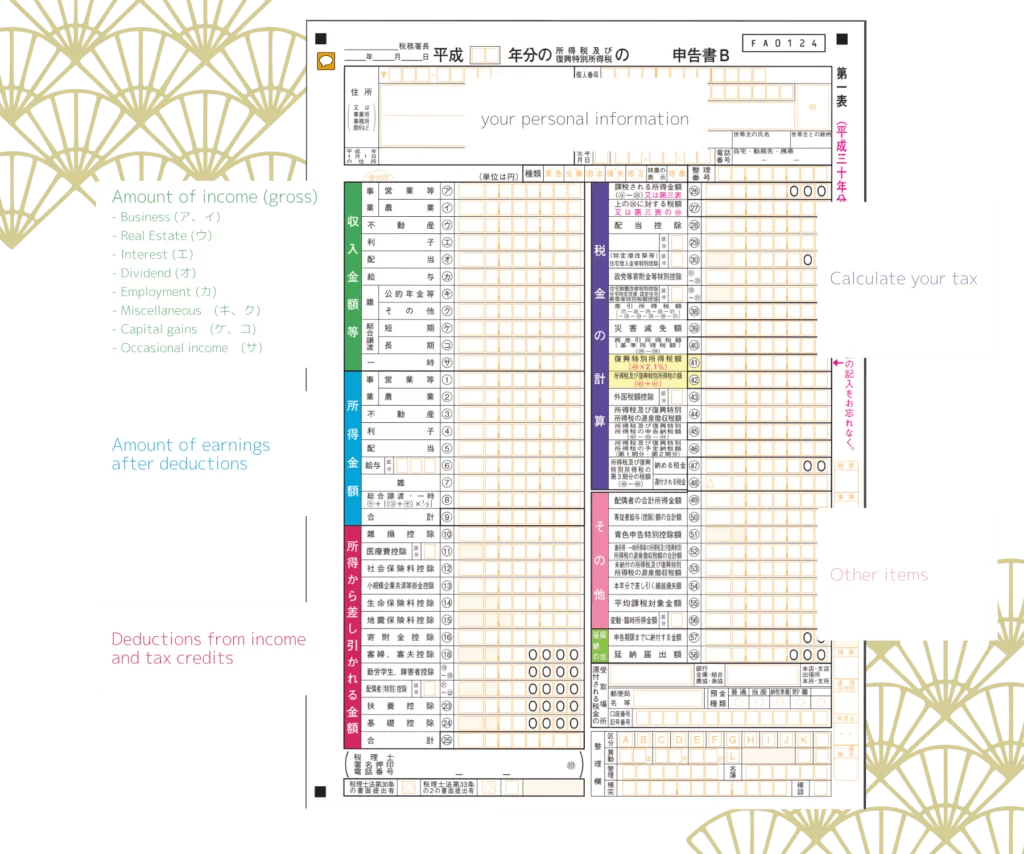

Japan's Income Tax Form

The income tax declaration form in Japan is called "Kakutei Shinkoku." The form consists of several sections where taxpayers need to provide detailed information about their income, expenses, deductions, and other relevant items.

Below is a summary of the main sections of the income tax declaration form in Japan:

- Taxpayer identification: This section includes personal information of the taxpayer, such as name, address, foreign registration number, among others.

- Income: In this section, the taxpayer needs to report all types of income received during the fiscal year, including salaries, investment income, rents, pensions, among others.

- Expenses: In this section, the taxpayer can declare their deductible expenses, such as medical expenses, contributions to pension plans, donations to charity, among others.

- Personal deductions: The taxpayer can request personal deductions for themselves and their dependents, which are calculated based on income and number of dependents.

- Withholding tax: This section includes information about the withholding tax on payments received throughout the fiscal year, such as salaries and pensions.

- Calculation of tax due: Based on the information provided in the previous sections, the tax authority calculates the tax due by the taxpayer.

- Tax payment: In this section, the taxpayer can indicate how they wish to make the payment of the tax due, which can be made in installments or in full.

What happens if income tax is evaded in Japan?

Tax evasion is an illegal practice and can have even more serious consequences than simply not paying income tax in Japan. Tax evasion occurs when the taxpayer omits information or falsifies documents to avoid paying taxes.

If a taxpayer is caught evading taxes, they may face the following legal and financial consequences:

- Fines and interest: The taxpayer may be fined up to 50% of the tax due, in addition to daily interest on the amount owed until payment is made.

- Criminal prosecution: Tax evasion is considered a criminal offense in Japan and can lead to criminal prosecution. The taxpayer may be summoned to appear in court and may be sentenced to imprisonment, additional fines, and court costs.

- Loss of reputation: Tax evasion can have a negative impact on the taxpayer's reputation. If they are convicted of tax evasion, it can harm their professional and personal image, which is very important in Japan.

- Asset seizure: The tax authority may seize the taxpayer's assets, such as bank accounts and real estate, to recover the amount owed.

- Prohibition of conducting business activities: In extreme cases, the tax authority may prohibit the taxpayer from conducting business activities until the debt is paid.

- Prohibition of leaving the country: In extreme cases, the tax authority may prohibit the taxpayer from leaving the country until the tax due is paid.

- Seizure of assets: If the taxpayer does not make the payment even after a court decision, the tax authority may execute an asset seizure order. This means that the authority can confiscate the taxpayer's assets, such as real estate, vehicles, investments, or other assets, until the amount owed is recovered.

Community

Comments

0 comments

There are no published comments in this language yet.

Send comment